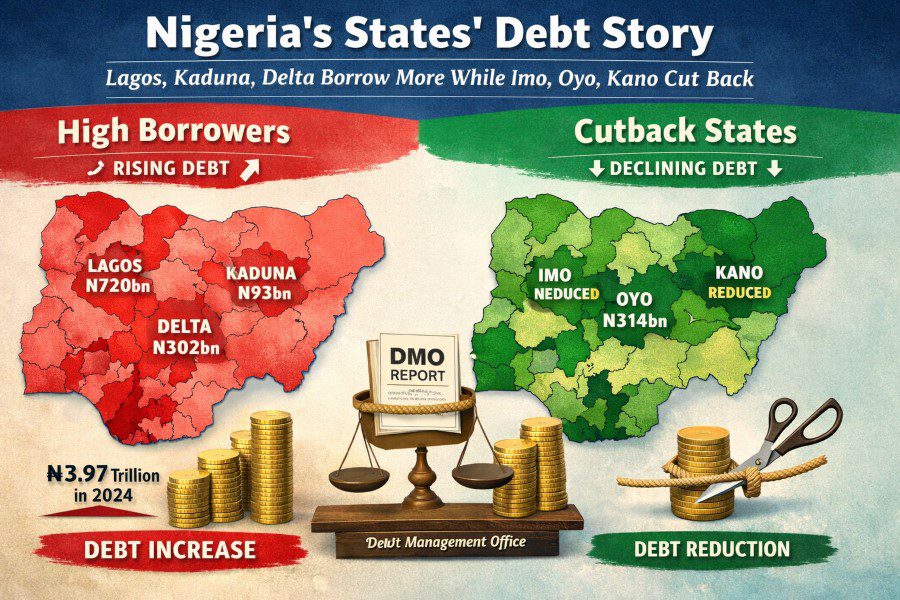

Nigeria’s subnational debt profile is entering a defining phase, shaped by widening contrasts in fiscal behaviour, rising borrowing pressures, and growing concerns about long-term sustainability. Fresh data from the Debt Management Office (DMO) shows that the domestic debt stock of Nigeria’s 36 states and the Federal Capital Territory (FCT) rose from N3.97 trillion in December 2024 to N4.36 trillion in December 2025.

This represents an increase of N392.41 billion within a single year—an unmistakable signal of persistent reliance on debt to bridge fiscal gaps at the subnational level.

At the heart of this development lies a dual reality. While some states are tightening fiscal discipline and reducing their debt exposure, others are expanding liabilities at a pace that raises questions about prudence, accountability, and long-term planning. This divergence is increasingly shaping Nigeria’s fiscal federalism narrative.

The data reveals a striking split. On one hand, 22 states recorded reductions in their domestic debt profiles, suggesting improved fiscal restraint or better revenue management. On the other hand, 14 states alongside the FCT recorded increases, driving the overall national rise in subnational indebtedness.

Imo State led the group of debt-reducing states with a decline of N42.40 billion, followed by Akwa Ibom (N37.35 billion), Bayelsa (N31.34 billion), Plateau (N26.59 billion), Edo (N21.82 billion), and Abia (N17.67 billion). Others such as Anambra, Benue, Adamawa, Kogi, Oyo, and Kano also recorded varying degrees of reduction.

These figures point to a quiet but important trend: some state governments are gradually improving fiscal discipline, possibly through enhanced internally generated revenue (IGR), tighter spending controls, and restructuring of existing obligations.

Yet this progress is counterbalanced by a more aggressive borrowing pattern in other states, which has pushed the aggregate debt figure upward.

Lagos, Kaduna, and the Rising Borrowers

Among the states that expanded their debt stock, Lagos stands out significantly with an increase of N319.27 billion—the highest in the federation. The Federal Capital Territory followed with N125.31 billion, while Kaduna recorded N58.88 billion, Delta N49.26 billion, Yobe N38.94 billion, and Enugu N38.32 billion.

Other states such as Cross River, Ogun, Borno, Rivers, Bauchi, and Kwara also added to their debt profiles, reflecting a broad-based borrowing trend across diverse regions and economic contexts.

Kaduna’s case is particularly notable due to its percentage increase of over 200 per cent, signalling either a sharp rise in financing needs or a significant shift in fiscal strategy.

Understanding the Drivers of Subnational Borrowing

The rising debt trajectory across many states is not occurring in isolation. It is largely driven by structural fiscal pressures that continue to define Nigeria’s subnational governance system.

First is the persistent mismatch between revenue and expenditure. Many states remain heavily dependent on statutory allocations from the Federation Account, which are often insufficient to meet rising wage bills, infrastructure demands, and social obligations.

Second is the infrastructure deficit. Roads, schools, healthcare systems, and public utilities require large-scale investment that exceeds the immediate fiscal capacity of most states. Borrowing therefore becomes a necessary tool to bridge development gaps.

Third is macroeconomic pressure. Inflation, currency depreciation, and rising interest rates have significantly increased the cost of governance and debt servicing, forcing some states to borrow even to maintain existing commitments

One of the most critical insights from the data is the concentration of debt in a small number of states. A handful of economically significant states account for a large share of total subnational debt, with Lagos alone representing a substantial proportion.

This concentration creates systemic vulnerabilities. Should revenue projections underperform or macroeconomic conditions worsen, the fiscal strain on these states could have broader implications for national economic stability.

It also raises questions about the efficiency of borrowing—whether debts are being channelled into productive investments capable of generating long-term returns or simply used to cover recurrent expenditure.

States that have reduced their debt profiles offer lessons in fiscal restraint. Their performance suggests that debt reduction is achievable when governments prioritise revenue expansion, curb non-essential spending, and adopt structured debt repayment plans.

However, the contrasting experience of high-borrowing states highlights a different reality—one where borrowing is increasingly used as a default response to structural revenue limitations.

This divergence is not merely statistical; it reflects differing governance philosophies, administrative capacity, and economic strategies across the federation.

Financial analysts have expressed concern that rising subnational debt may not always correspond with visible developmental outcomes. In some cases, there is limited evidence of proportional infrastructure expansion or economic transformation relative to the scale of borrowing.

This raises broader governance questions about transparency, accountability, and the efficiency of public financial management systems. Without strong oversight, borrowing risks becoming a short-term fix rather than a development tool.

There is also concern about weak linkage between debt acquisition and project performance evaluation. In many cases, borrowing decisions are not sufficiently tied to measurable outcomes, making it difficult to assess effectiveness.

The Federalism Dilemma

Nigeria’s fiscal federal structure remains a central factor in the debt conversation. States are constitutionally responsible for development, yet their revenue-generating capacity is uneven and often limited.

This imbalance creates a dependency cycle where borrowing becomes a structural necessity rather than a strategic choice. Until states achieve greater fiscal autonomy through improved tax systems and diversified economies, reliance on debt is likely to persist.

Calls for reforms in revenue allocation, improved fiscal transparency, and stricter borrowing frameworks continue to grow louder.

Addressing Nigeria’s subnational debt challenge requires more than caution—it demands structural reform. States must prioritise expanding their internal revenue base through modern tax systems, digital collection platforms, and improved compliance mechanisms.

Borrowing must also be more tightly linked to productive investments that generate economic returns. Infrastructure financing, if properly managed, can stimulate growth and improve future revenue capacity, but only when accompanied by strong project monitoring systems.

At the federal level, institutions such as the DMO must continue strengthening oversight mechanisms to ensure that borrowing remains within sustainable limits. Equally important is the need for greater transparency in how borrowed funds are utilised.

Civil society, the media, and citizens also have a role to play in demanding accountability and tracking the impact of public debt on development outcomes.

Conclusion: Debt as Tool or Trap

Nigeria’s state-level debt story is ultimately one of balance—between development ambition and fiscal caution, between immediate needs and long-term sustainability.

The rise in borrowing across several states reflects real developmental pressures, but also exposes structural weaknesses in revenue generation and public financial management.

As some states demonstrate fiscal discipline while others expand debt aggressively, the challenge becomes clear: ensuring that borrowing remains a tool for development rather than a pathway to fiscal strain.

The future of Nigeria’s subnational economy will depend not only on how much is borrowed, but more importantly on how wisely, transparently, and productively those funds are deployed.

Nigeria’s State Debt Landscape: Between Fiscal Discipline, Rising Borrowing Pressures